Mercado Libre: Latin America's Compounding Machine 2026 Deep Dive

How MercadoLibre turned a regional vacuum into an $80 billion business — and what the next decade looks like

Prefer to listen? The audio walkthrough covers the key points, but the full analysis — data, charts, and scenario models — lives in the article below.

Disclaimer: This report is for informational and educational purposes only and does not constitute investment advice, a recommendation, or a solicitation to buy or sell any security. The author may hold positions in securities discussed. Past performance is not indicative of future results. Readers should consult a qualified financial advisor before making any investment decisions. Do your own research.

Contents

Latin America in 1999

When Marcos Galperin sketched the business plan for MercadoLibre Inc. while at Stanford University in 1999, the regional landscape lacked almost every structural pillar that US internet pioneers took for granted.

Regional internet penetration was stuck in the low single digits. Banking was a luxury reserved for the affluent; the vast majority of adults operated strictly in cash, and credit cards were a rarity outside wealthy urban enclaves. Reliable, low-cost home delivery was essentially non-existent.

While an American e-commerce startup could simply plug into Visa, outsource shipping to UPS, and assume its target market possessed bank accounts, replicating that playbook in Latin America would have confined the business to the thin upper slice of the population that already had those things. To capture the region's vast, underserved population, MercadoLibre realized it would have to build its own payments infrastructure, its own logistics network, and its own credit arm.

That massive infrastructure buildout effectively _became_ the company. Every layer added since can be viewed as an ambitious effort to push deeper into the mass market, bringing lower-income consumers into the digital formal economy.

Founding and the competitive vacuum

Galperin’s foundational thesis was straightforward: a localized champion would inherently outmaneuver any US tech giant attempting to export a domestic playbook into markets it did not comprehend.

Launching from a Buenos Aires garage on August 2, 1999, alongside co-founders Hernán Kazah and Stelio Tolda, the startup captured 15,000 users and $2 million in gross sales within its first 90 days.

While the early landscape was highly fragmented—featuring roughly 80 well-capitalized dot-com contenders—the subsequent market crash systematically cleared the field. MercadoLibre survived by prioritizing sustainable unit economics over subsidized growth.

A pivotal 2001 alliance with eBay Inc., which took a minority stake and handed over its Brazilian operations in exchange for a non-compete agreement, neutralized its most formidable global threat during its vulnerable early years. Meanwhile, Amazon.com Inc. delayed its entry into Brazil’s marketplace until 2012, and didn't roll out its Prime ecosystem there until 2019. This afforded MercadoLibre a nearly 20-year uncompetitive runway to entrench itself as Latin America’s dominant commerce platform.

From auctions to a marketplace

Originally structured as a consumer-to-consumer auction house modeled on early eBay, MercadoLibre shifted toward a fixed-price marketplace model in the mid-2000s. This transition allowed established merchants selling new inventory to scale on the platform. By its 2007 initial public offering, fixed-price transactions surpassed auctions, eventually accounting for roughly 95% of total sales. This evolution unlocked the scale necessary to justify heavy capital investments in proprietary payments and logistics.

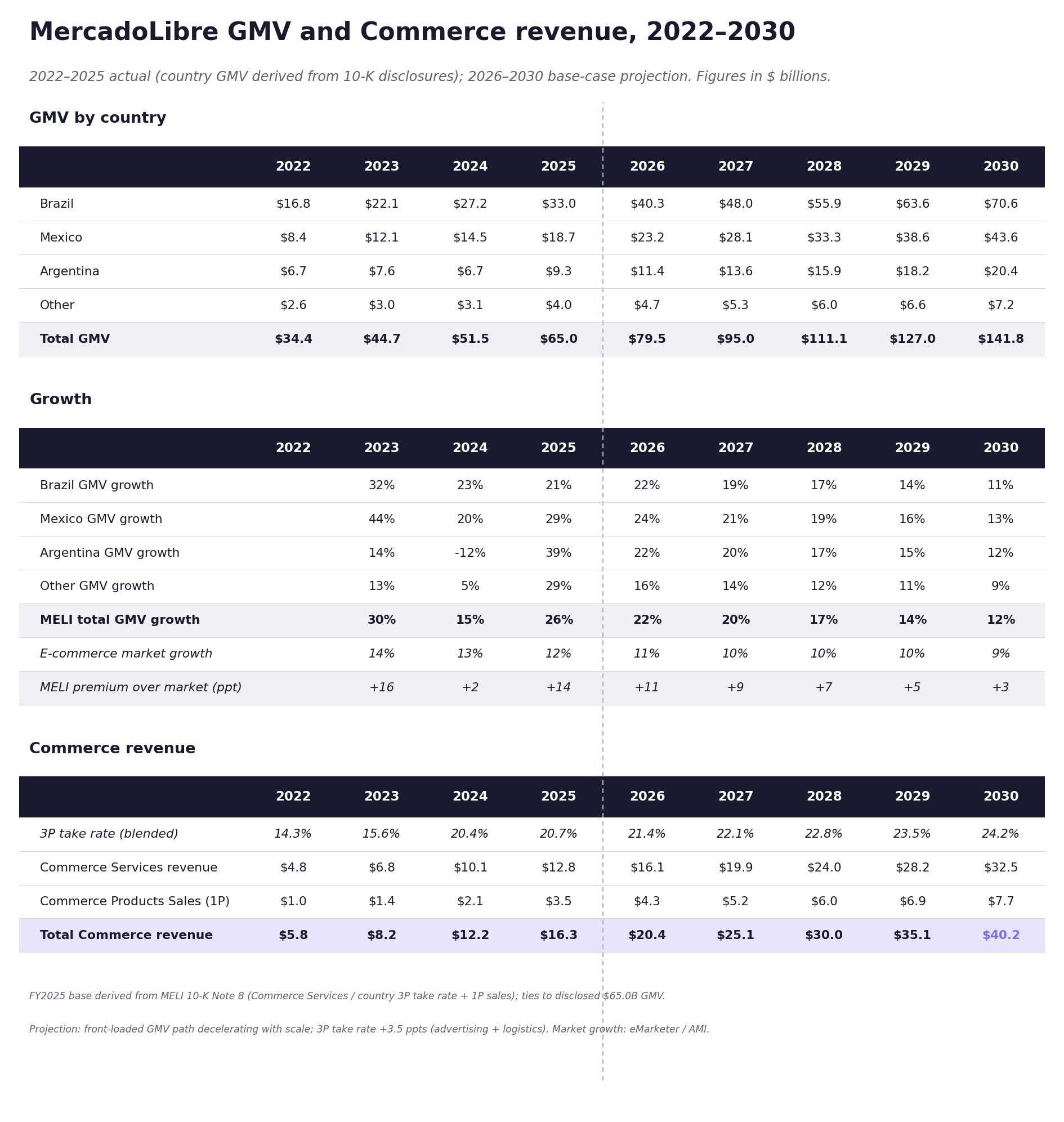

Today, the Commerce division operates a highly efficient, capital-light third-party (3P) marketplace, which generates over 90% of its $65 billion in Gross Merchandise Volume (GMV). MercadoLibre collects a steady 20% to 21% take rate on these transactions. It supplements this core with a targeted first-party (1P) retail business for high-barrier categories like electronics, alongside a rapidly expanding retail media arm, Mercado Ads.

Building the infrastructure: payments, delivery, and lending

If commerce is MercadoLibre's consumer face, Mercado Pago is its financial plumbing. Launched in 2003, the payments network was engineered around an idiosyncratic regional reality: its users did not have bank accounts.

Unlike PayPal, which simply routed money between existing bank accounts, Mercado Pago built a hybrid digital-cash network. It established partnerships with neighborhood pharmacies and convenience stores, allowing unbanked consumers to pay for online purchases with physical cash at a local counter. Once the agent verified the cash receipt, MercadoLibre cleared the transaction and prompted the seller to ship.

Starting in 2015, the company aggressively expanded Mercado Pago beyond its own marketplace, distributing low-cost point-of-sale (mPOS) card readers and QR codes to brick-and-mortar merchants. By 2019, off-platform payment volume eclipsed marketplace volumes. Mercado Pago has since evolved into a comprehensive digital wallet ecosystem, allowing users to hold balances, pay utility bills, and access asset management tools.

Fintech revenue is now split almost evenly between traditional transaction processing and its high-margin credit division, Mercado Crédito.

Launched in 2017 after internal metrics revealed that three-quarters of the platform’s merchants lacked access to traditional banking credit, Mercado Crédito leverages an information asymmetry that traditional banks cannot replicate. Because merchant sales flow directly through Mercado Pago, MercadoLibre has real-time visibility into cash flows and risk profiles. Crucially, it intercepts loan repayments directly from daily merchant sales before those funds ever hit the seller’s bank account.

The recent sell-off

Despite compounding net revenues twentyfold since 2018 to $28.9 billion in 2025, MercadoLibre’s stock has recently experienced downward pressure. The primary catalyst is a compression in headline operating margins, which fell from the mid-teens in 2023 to roughly 10% in 2025, and touched 6.9% in the first quarter of 2026.

A granular analysis of the income statement reveals this margin compression is driven by accounting treatments and deliberate strategic investments, rather than core operational degradation:

Credit Provisioning (Approx. Two-Thirds of Decline): Under prevailing accounting standards, MercadoLibre must recognize a loan's lifetime expected credit losses the moment it originates, well before it generates any interest income. With the gross loan book growing at a blistering 87% annualized clip—reaching $12.5 billion in 2025—the reported margins are systematically depressed by front-loaded provisions.

Logistics Reinvestment (Approx. One-Third of Decline): The company has aggressively lowered its free-shipping thresholds in key regions like Brazil and expanded its fulfillment footprint, operating 22 logistics hubs in Brazil alone.

This capital-intensive infrastructure cycle mirrors the classic mid-career strategy of Amazon: sacrificing near-term margins to build an unassailable logistics moat that drives long-term transaction volume.

Business Segments

MercadoLibre structures its financial reporting around two primary operational engines: Commerce and Fintech. While the e-commerce marketplace spans an 18-country footprint, its financial services arm, Mercado Pago, operates across eight nations. Crucially, both segments leverage a singular, unified user base and a shared data infrastructure, creating a powerful ecosystem cross-sell effect.

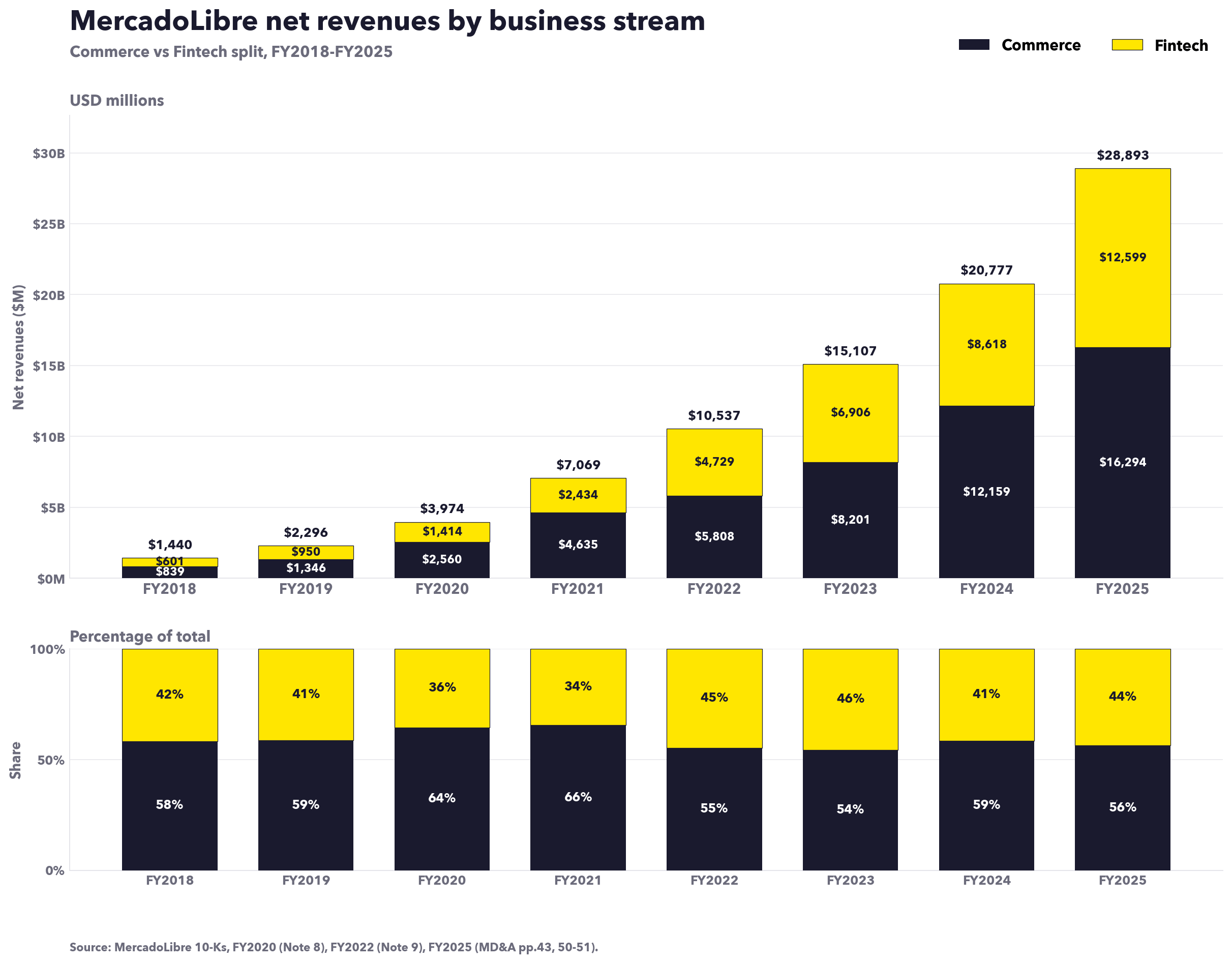

Charts: MercadoLibre 10-Ks, FY2020 Note 8, FY2022 Note 9, FY2025 MD&A pp.43, 50-51. Commerce vs Fintech disclosure begins FY2018; earlier filings reported revenue by geography only, with payments commissions embedded in each geographic segment.

The Commerce stream

MercadoLibre operates the undisputed heavyweight of Latin American e-commerce. In fiscal year 2025, the marketplace processed $65.0 billion in Gross Merchandise Volume (GMV), translating to 2.4 billion items sold to 121 million unique active buyers. This performance represents roughly a fivefold expansion in GMV since 2018.

Sell-side estimates peg MercadoLibre’s regional market share in the mid-to-high 20% range of total online retail—effectively commanding a larger market share than its next 11 competitors combined. The company maintains the No. 1 digital retail position in Brazil and Argentina, and runs neck-and-neck with Amazon.com Inc. in Mexico.

The operational blueprint replicates the Amazon model but modifies it for regional capital efficiency:

Third-Party (3P) Marketplace: The core business is strictly capital-light, hosting independent merchants who account for more than 90% of total GMV.

First-Party (1P) Retail: Direct inventory ownership is deployed defensively, serving as a targeted tactical patch to guarantee supply in specific high-barrier categories like electronics and groceries.

Logistics & Advertising: The core platform is reinforced by an in-house delivery network (Mercado Envíos) and a high-margin retail media arm (Mercado Ads).

This 3P-heavy strategy is a deliberate hedge against regional macro risks. In inflation-prone economies where capital costs run high, leaning on independent merchant inventory shields MercadoLibre's balance sheet from excessive capital expenditure.

Mercado Envíos, the logistics arm, runs through fulfillment centers plus a network of partner pickup and drop-off points called MELI Places: corner stores and pharmacies that handle the last mile and returns.

The Fintech stream

MercadoLibre’s financial services arm, Mercado Pago, has emerged as one of the most powerful digital banking forces in Latin America. Monthly active users surged from 35 million in fiscal year 2022 to 78 million by fiscal year 2025.

Despite this blistering growth, the company has tapped only a fraction of its total addressable market. Its current user base accounts for roughly 20% of the 390 million adults across its primary operating territories—a region where close to 70% of the population was classified as unbanked or underbanked as recently as 2019.

Mercado Pago's strongest position, as in commerce, is Argentina, where it leads digital payments by a wide margin. Brazil, Mexico, and Chile are more competitive.

To optimize the user experience, the fintech business operates via a dedicated Mercado Pago app, distinct from the core Mercado Libre e-commerce application. However, the two platforms remain tightly integrated through a single digital identity framework:

Unified Account Access: Users share a single login, payment profile, and data record across both apps.

Loyalty Integration: The company's premium subscription tier, Meli+, spans both ecosystems to eliminate friction as users transition from consumer retail to digital banking.

The Digital Account: The platform functions as a comprehensive dashboard allowing consumers and commercial enterprises alike to store capital, execute peer-to-peer transfers, and access credit.

The Dual-Pillar Business Model

1. Payments and Float Income

This segment monetizes transaction volumes through merchant card processing fees, peer-to-peer transaction tolls, point-of-sale (mPOS) terminals, and QR code network fees. It also captures net interest income by investing the "float"—the cash balances left sitting inside Mercado Pago consumer accounts.

FY2025 Total Payment Volume (TPV): $277.8 Billion

Merchant Acquiring (Off-Platform Store Processing): $188.1 Billion

Consumer App Payments: ~$90.0 Billion

FY2025 Segment Revenue: $6.7 Billion (representing 53% of total Fintech top line)

2. Credit (Mercado Crédito)

Operating under the proprietary Mercado Crédito banner, this division manages a diverse financing book spanning credit card originations, cash advances for consumers, and short-term working capital facilities for corporate merchants.

FY2025 Gross Loan Book: $12.5 Billion

Credit Cards: $5.7 Billion (the fastest-growing product line inside the entire corporate portfolio)

Consumer Loans: $4.6 Billion

Merchant Working Capital: $2.0 Billion

FY2025 Segment Revenue: $5.9 Billion _(representing 47% of total Fintech top line)

The long-term investment case for Mercado Pago rests on a secular, structural shift from cash to digital rails across Latin America. While the payments segment scales by migrating everyday physical cash transactions onto digital networks, the credit arm grows by capturing high-margin interest income from a consumer and small-business base long abandoned by traditional legacy banks.

The Structural Advantage: The competitive advantage stems from a closed-loop data flywheel. Core e-commerce and merchant processing activities generate vast amounts of real-time behavioral data. This proprietary data directly feeds Mercado Pago's underwriting models, allowing the company to price credit risk with high precision. As credit is extended, it flows directly back into the system, driving higher transaction volumes across the payment network. It is an operational loop that traditional commercial banks cannot easily replicate because they lack visibility into the underlying merchant commerce.

What has driven the growth so far

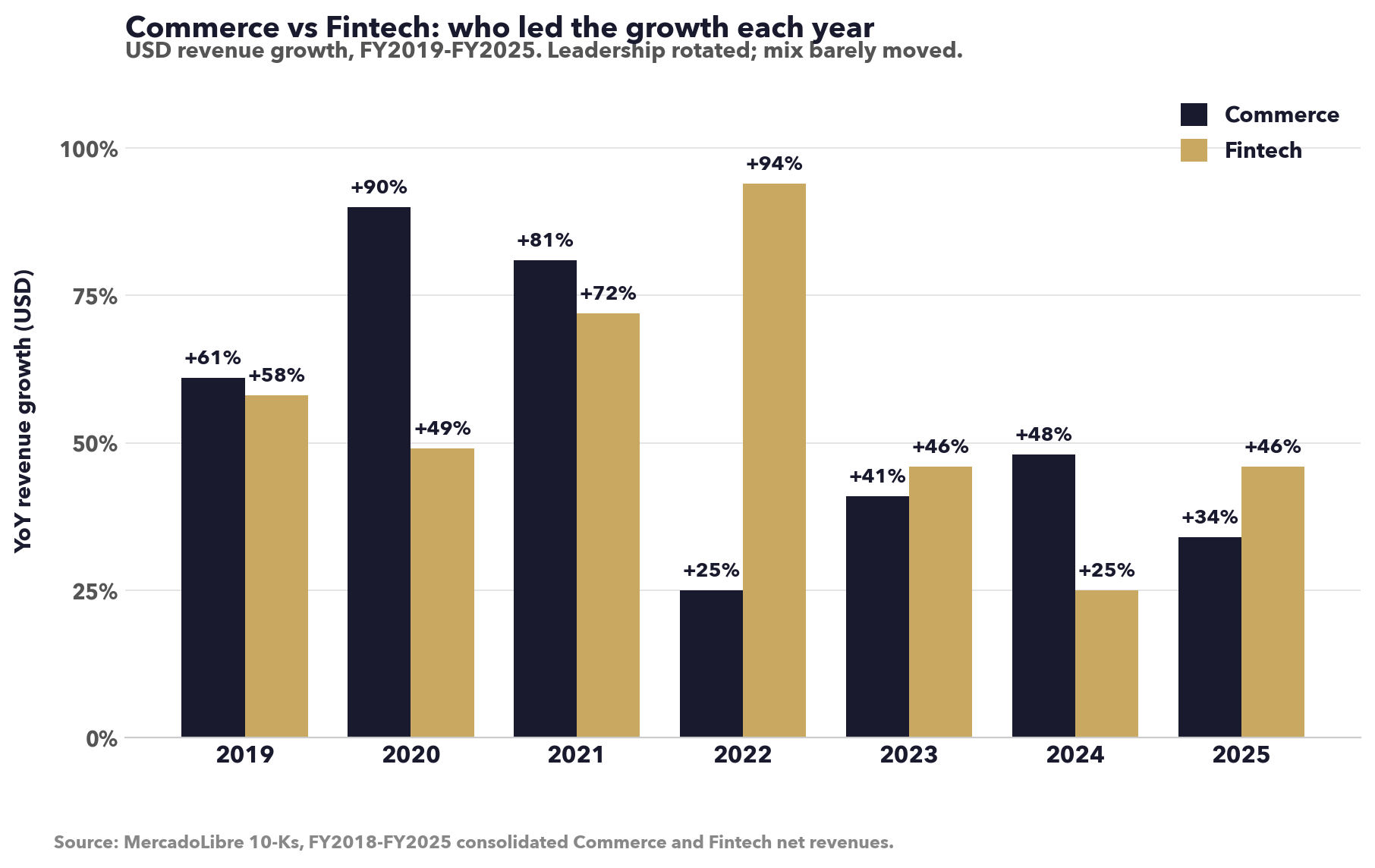

Revenue has compounded at roughly 53 percent a year since 2018, and the two segments have grown in lockstep. Commerce and Fintech each rose about 20x over the period, and the revenue mix barely moved: Commerce was 58 percent of the total in 2018 and 56 percent in 2025.

The growth model within the retail unit relies on two distinct compounding levers: expanding gross marketplace volume and increasing the take rate on every dollar processed. GMV grew ~5x since 2018 while Commerce revenue grew ~19x; the gap is take-rate expansion.

Volume: items sold grew 7.3x, from 335 million in 2018 to 2.4 billion in 2025, roughly 33 percent a year. Two forces drove it:

More buyers, buying more often. Unique active buyers rose from 74M in 2022 to 121M in 2025; items per buyer climbed from about 15 to about 20. Free shipping was the main pull, alongside broader payment access: By leveraging the Mercado Pago digital wallet and proprietary consumer credit lines, the company systematically onboarded cash-reliant demographics who previously lacked the financial plumbing to participate in digital commerce.

Faster, cheaper delivery. The share of items delivered within 48 hours went from 21 percent in 2017 to 76 percent by early 2026, and the mid-2025 cut in Brazil's free-shipping threshold lifted items sold 56 percent year over year.

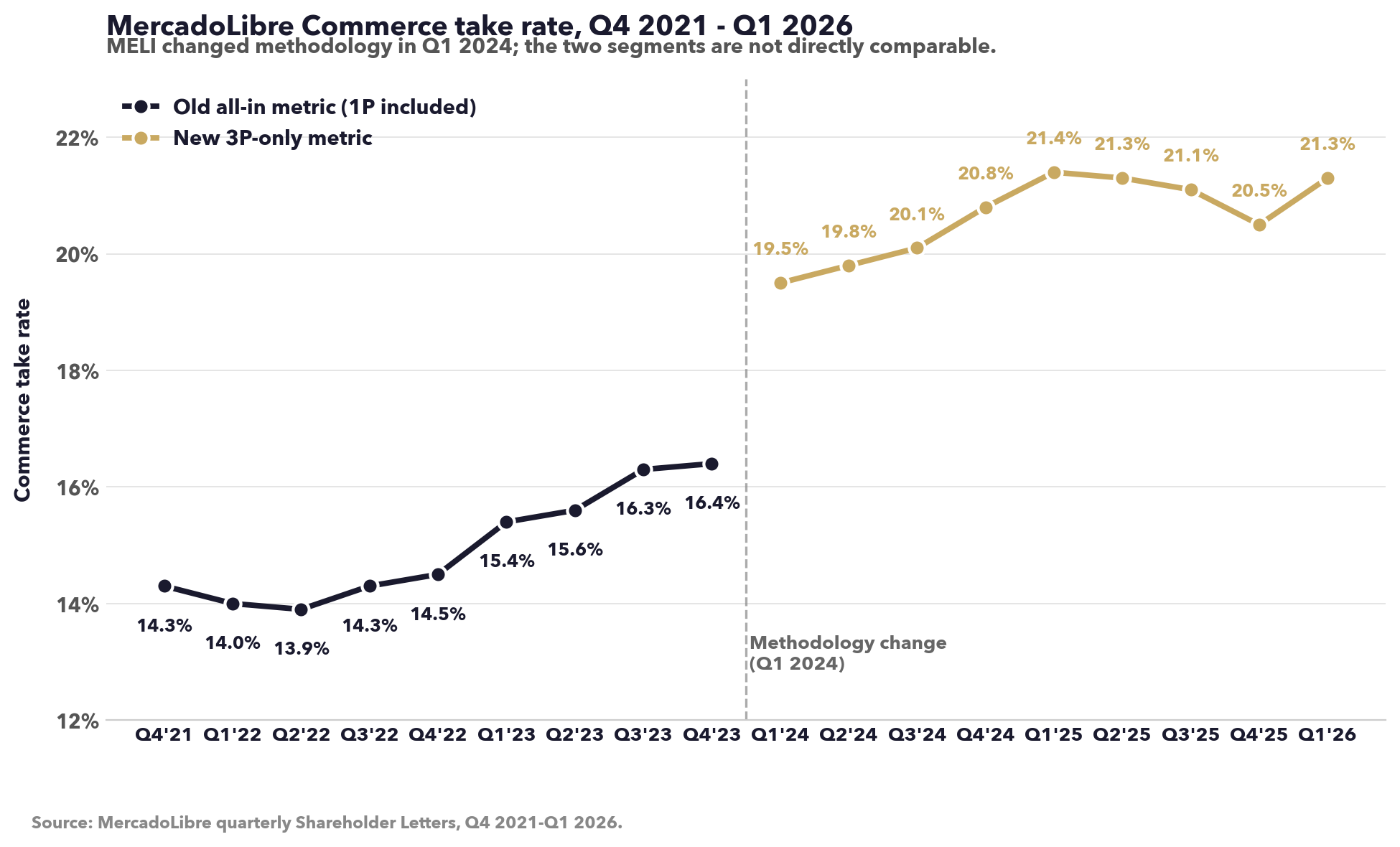

Take rate: Commerce revenue as a share of GMV rose from the mid-teens to about 21 percent. The core seller commission has held flat since 2023; the gain came from value-added services layered on top:

Advertising is the standout. Mercado Ads represents the primary margin catalyst. Ad revenue as a share of total GMV rose from a nominal 0.5% in 2019 to 2.0% in 2024. Given that Amazon’s mature digital ad load hovers near 7%, MercadoLibre retains a long, highly profitable runway for ad expansion.

Ancillary Fee Layers: Fixed per-listing transaction fees and recurring subscription revenue from the Meli+ ecosystem provided secondary, incremental support to the overall take-rate uplift.

One caveat: a Q1 2024 accounting change inflated the reported take rate by about 2.6 points without changing the economics, so the headline jump overstates the real move.

Inside Fintech, the story has rotated from payments to credit.

Payments: total payment volume grew 15x to $277.8 billion, as Mercado Pago grew from handling checkout on MercadoLibre's own marketplace to processing payments for merchants across the wider economy: physical shops and other websites, through card readers, QR codes, and online checkout.

Transaction Volume: Absolute payment counts grew 40-fold, skyrocketing from 389 million in 2018 to 15.5 billion in 2025.

Ticket Sizes: Because transaction frequency outpaced total dollar volume growth, the average payment size shrank significantly. This indicates that Mercado Pago has successfully embedded itself into low-ticket, everyday consumer spending.

User Base: Monthly active users (MAUs) more than doubled over a three-year period, rising from 35 million in 2022 to 78 million in 2025.

Credit: the gross loan book went from $2.8 billion to $12.5 billion since 2022, becoming the marginal growth driver.

Credit cards: up 9.3x to $5.7 billion, now 45 percent of the book versus 22 percent three years ago.

Consumer loans: grew to $4.6 billion; merchant working capital to $2.0 billion.

The card rollout is staggered: Brazil 2021, Mexico 2023, Argentina 2026.

The growth runway

Headline numbers:

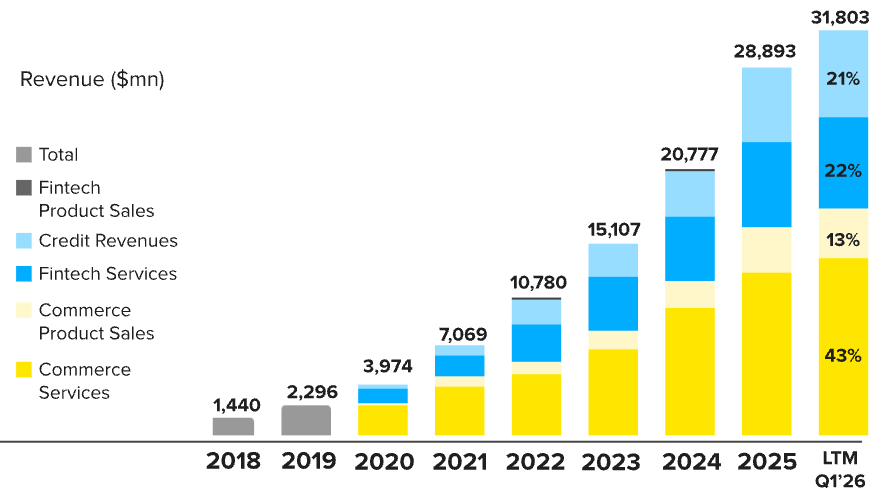

2025 revenue: $28.9 billion, up from $1.4 billion in 2018 — a 20x in seven years.

Q1 2026 growth: 49% year over year.

Segment mix: Commerce 56%, Fintech 44%; essentially unchanged since 2018, when the split was 58/42.

2025 revenue by country:

Brazil: $15.2 billion — largest market.

Mexico: $6.5 billion — the fastest-growing of the three.

Argentina: $6.0 billion — most profitable, at roughly three times Brazil's margin.

2025 e-commerce penetration (online sales as a share of total retail) across MercadoLibre's three core markets:

Mexico: ~17%.

Brazil: ~11%.

Argentina: <10%.

For reference, the US sits at ~16% and China at ~26%.

The 20x is history. The question is what the run rate settles at over the next decade, and the answer mostly turns on those penetration figures. Internet penetration across MercadoLibre's markets already averages above 80 percent, so the next decade is not about new users coming online. It is about e-commerce taking share from offline retail.

How fast that share moves depends on what online has to compete with. The US took close to two decades to climb from 1 percent penetration to 11 percent, because online had to wrestle share from an entrenched physical retail base of national chains and big-box stores. China went from 11 percent to 25 percent in about five years, because organized retail outside the largest cities was thin and there was little incumbent infrastructure for online to displace. Latin America's setup looks closer to China's: the retail base is fragmented across small informal merchants rather than anchored by national chains, leaving more share for online platforms to take. A mid-twenties terminal supports close to another decade of double-digit dollar growth.

The forward case rests on four drivers, two in each segment. In Commerce, they are GMV and the take rate.

1. GMV Trajectory: Structural Share Gains With Scaled Deceleration

The base-case valuation model projects robust near-term volume expansion anchored by recent performance, followed by a gradual multi-year deceleration as the market matures.

When mapped top-down against the broader regional landscape—where Latin American e-commerce is forecast to grow at a 9% to 12% compound annual rate—MercadoLibre is structurally positioned to continue capturing market share. However, its operational alpha over the broader industry is modeled to narrow sequentially over time.

Brazil and Mexico are the steady engines, both compounding GMV in the low-to-mid 20s with no sign of slowing. Their paths start there and taper toward low double digits by 2030.

Argentina slows the fastest. Its recent growth was lifted by the country's economic rebound and high inflation; as both normalize, Argentine growth comes down.

2. Take-Rate Optimization:

Take rate. The take rate is the share of each GMV dollar that MercadoLibre keeps as revenue. The base case lifts it by roughly 3.5 percentage points by 2030, from two add-on services:

Advertising: ad revenue is about 2 percent of GMV today against roughly 7 percent at Amazon, and the base case closes part of that gap.

Logistics: MercadoLibre barely charges for its delivery network today. As that network matures, the company can begin monetizing it, the way Amazon does with fulfillment.

The basic seller commission has not changed since 2023 and is assumed to stay flat, so the increase comes from these services, not from charging sellers more.

Put together, Commerce GMV grows from $65 billion to $142 billion by 2030, a 17 percent CAGR. The annual rate is front-loaded and steps down each year: 22 percent in 2026, 20 percent in 2027, 17 percent in 2028, 14 percent in 2029, and 12 percent in 2030. Commerce revenue reaches $40 billion, a 20 percent annual rate, running ahead of GMV because of the take-rate expansion.

That path is still a step down from the record: MercadoLibre's GMV compounded at 24 percent a year from 2022 to 2025. The base case assumes that pace decelerates as the company gets larger and Argentina's inflation tailwind fades, rather than holding flat.

The rest of this report is for paid subscribers.

What's behind the paywall:

The Fintech growth runway — the wallet, payments, and credit-book projections

The full valuation — the discounted-cash-flow model and what MercadoLibre is worth

The risks — Argentina, the credit book, regulation, and competition

The complete Excel model — every assumption and projection in this report